Many eCommerce store owners treat payment processing as a simple, interchangeable utility, believing that selecting a solution is just a matter of finding the lowest advertised transaction fee. This assumption is the first, silent leak in your revenue funnel. By treating the core checkout experience as a commodity, you forfeit crucial control over transaction routing, customer data, and the ability to customize the final mile of the buyer’s journey. This operational passivity inevitably leads to spiraling hidden costs and non-negotiable fees, actively hemorrhaging future Customer Lifetime Value (LTV) with every sale processed through a restrictive system.

The complexity of high-growth eCommerce is not in accepting a credit card, but in understanding the distinct, profit-driven functions of a payment gateway, a payment processor, and a payment aggregator. A mistaken choice among these three is not merely an administrative error—it’s a systemic technical limitation that dramatically stunts your ability to execute critical revenue expansion strategies, such as optimizing checkout conversion or fueling high-impact email/SMS flows with real-time transactional data. This is the definitive guide to moving beyond transactional confusion and strategically selecting the payment infrastructure that is fundamentally engineered to maximize your store’s scalability and long-term profitability.

Maximize Checkout Conversion: Choosing the Right Payment Gateway Architecture

The selection of your payment gateway architecture is not a backend technical detail; it is a critical, conversion-driving factor. Cart abandonment studies consistently show a measurable drop in completed sales when the customer is forced to leave the store’s domain—even briefly—to process a payment. To maximize checkout conversion, high-growth WooCommerce stores must prioritize an ‘on-site’ or ‘direct’ integration that allows the entire transaction to be completed without redirecting the user, thereby maintaining trust and a seamless brand experience.

- Redirect Gateway: Redirects the customer to the gateway’s external page to enter payment details.

- Conversion Impact: Higher abandonment rate due to flow disruption and a break in the established site trust.

- Direct/On-Site Gateway: Payment fields are embedded directly into the WooCommerce checkout page using secure methods like hosted fields or tokenization. Conversion Impact: Provides a frictionless, high-trust experience that is essential for maximizing your conversion rate and Average Order Value (AOV).

The strategic choice is the direct architecture, which places the security onus on your gateway provider via tokenization to minimize your PCI compliance scope. By keeping the customer on your checkout page, you retain crucial control over the final moments of the journey. This control allows for the optimization of checkout fields, the strategic inclusion of trust badges, and the integration of last-mile offers, turning the checkout from a functional necessity into a powerful, revenue-generating part of your funnel.

Leveraging Processor Data to Trigger High-Converting Email/SMS Flows

The strategic advantage of selecting a high-quality payment processor lies in the rich, granular transaction metadata it generates, which is often severely underutilized in post-purchase marketing. For a WooCommerce store focused on maximizing Customer Lifetime Value (LTV), the goal is to integrate the processor’s API or webhooks with the marketing automation platform (ESP/CRM). This technical synchronization allows you to move beyond basic ‘transaction successful’ or ‘transaction failed’ triggers, enabling the creation of hyper-contextualized email and SMS flows that address the precise nature of the customer’s interaction.

By leveraging specific, high-intent signals transmitted by the processor, you can deploy precision-targeted flows that dramatically improve payment recovery rates and deepen customer loyalty:

- Specific Soft Decline Codes: Description: Use transient decline codes (e.g., ‘Insufficient Funds’ or ‘Transaction Timed Out’) to trigger an immediate, empathetic SMS or email directing the customer back to the checkout with a small, time-sensitive incentive, recovering sales lost due to temporary issues.

- Payment Method Type Used: Description: Segment post-purchase nurture sequences based on the initial payment method—target customers who used Buy Now, Pay Later (BNPL) with information on other installment-eligible products, or offer faster shipping to repeat customers paying with a saved, trusted credit card.

- Successful Authorization/Pre-Order Confirmation: Description: Distinguish between the ‘authorized’ status (for delayed shipping/pre-orders) and ‘captured’ status to send highly accurate and distinct fulfillment updates, which manages customer expectation and reduces support inquiries during the waiting period.

This technical rigor in utilizing processor data transforms your communication strategy from reactive to predictive. By ensuring your marketing messages are directly informed by the real-time financial status and payment behavior of the customer, you minimize friction at critical stages of the customer journey and turn potential churn points—like a failed subscription payment—into opportunities for high-converting re-engagement.

Automating Transaction Workflows: Aggregators vs. Traditional Processors for Scale

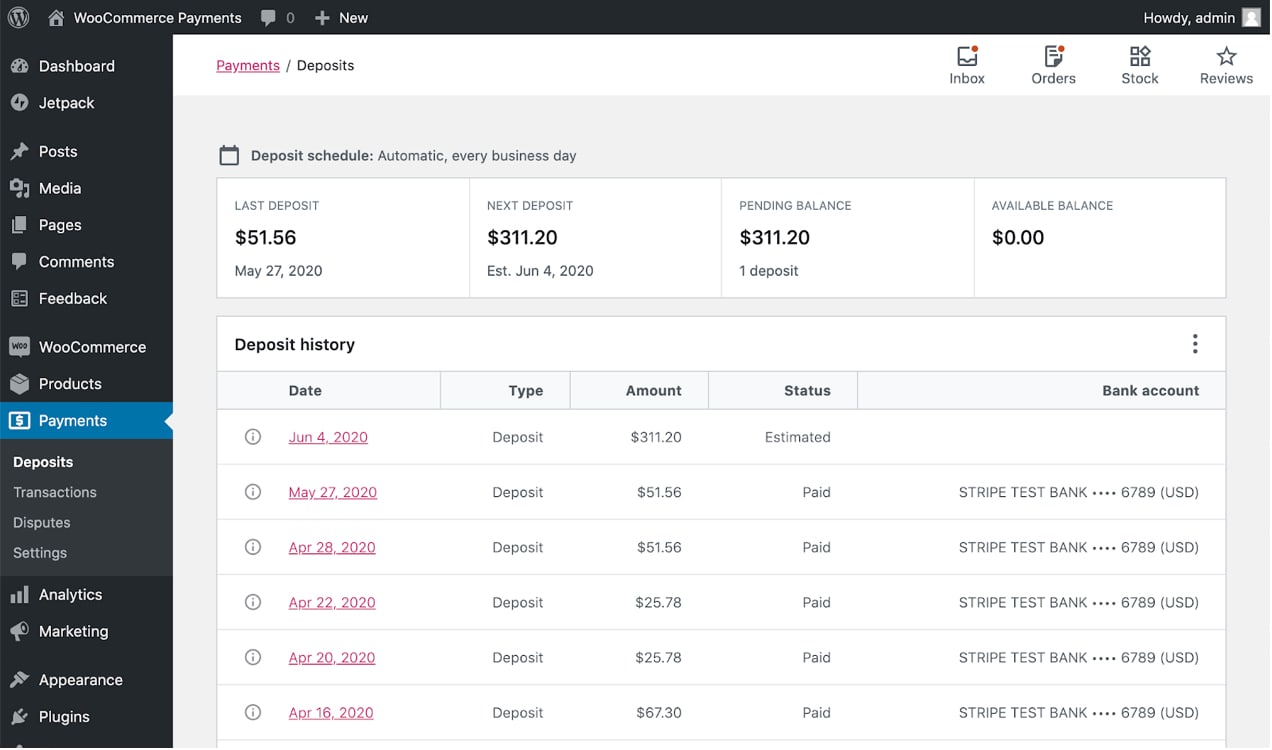

For a scaling WooCommerce store, the choice between a Payment Aggregator (like Stripe or PayPal) and a traditional Processor/Gateway model is a critical architectural decision that directly impacts the scalability and security of your financial workflows. Aggregators offer immediate ease of use: they act as the merchant of record, streamlining the entire transaction process into a single, unified API. This simplicity accelerates time-to-market and simplifies initial reconciliation. However, this same centralization means you have less control over core transaction elements, which can limit your ability to optimize complex flows and manage risk as your volume accelerates.

The true difference emerges when implementing sophisticated transaction automation required for global or high-volume growth. A traditional processor model, which pairs a dedicated merchant account with a separate gateway, provides the technical flexibility to automate high-level financial operations that aggregators abstract away.

- Aggregator Efficiency: Provides rapid onboarding and centralized data via unified APIs, which speeds up initial reconciliation but introduces a critical single point of failure and limited control over bank-level underwriting.

- Traditional Processor Control: Requires complex initial setup, but offers a direct banking relationship for customized transaction routing and dedicated risk management, essential for optimizing high-value and multi-currency approval flows.

- Financial Automation: Aggregators simplify basic webhooks for immediate events (payment/refund). Traditional setups enable deeper ERP and accounting system integration necessary for automating granular, high-volume financial reconciliation and tax compliance across different jurisdictions.

Scaling past seven-figure annual revenue requires a strategic pivot toward payment orchestration, which is only genuinely possible with a traditional or hybrid model. By not being locked into a single processor’s risk management rules, you can automate intelligent transaction cascading and failover logic. This minimizes revenue loss from false declines, provides superior chargeback defense workflows, and enables automated multi-currency settlement optimization—turning your payment architecture from a bottleneck into a resilient, globally automated financial system.

Hidden Costs and Fee Structures: Protecting Your Ecommerce Profit Margin

The true cost of accepting payments extends far beyond the advertised transaction percentage. For high-volume WooCommerce stores, a superficial comparison between a flat-rate payment aggregator and an interchange-plus model with a dedicated processor can mask significant margin erosion. Aggregators offer simplicity but often charge a hidden premium for lower volume transactions and impose rigid reserve structures. Conversely, a custom-tiered solution, while appearing complex, can yield a far lower effective rate at scale, provided the merchant meticulously audits the non-transactional fees. These ancillary charges—often buried in the fine print—are the silent killers of eCommerce profitability.

- Interchange Fees: The cost paid to the customer’s card-issuing bank, which varies based on card type (e.g., rewards, corporate) and is a non-negotiable pass-through expense.

- Assessment Fees: Network fees charged by card brands (Visa, Mastercard, etc.), which are typically a small percentage and fixed fee per transaction.

- Gateway Fees: A monthly fee or a per-transaction micro-fee charged by the gateway for securely routing and encrypting the payment data to the processor.

- Chargeback Fees: A significant fixed cost imposed by the processor or aggregator every time a chargeback is initiated, regardless of whether the merchant wins or loses the dispute.

- PCI Compliance Fees: Annual or monthly fees for ensuring and validating that the store meets the diretrizry Payment Card Industry Data Security Standard (PCI DSS) requirements.

The actionable path to margin protection is calculating your effective rate—your total monthly processing costs divided by your total monthly sales volume. This single metric provides a clear, apples-to-apples comparison between any two providers. For a scaling WooCommerce business, the optimal strategy pivots on transaction volume and Average Order Value (AOV). While flat-rate aggregators offer immediate ease, once volume scales past a certain threshold, transitioning to a processor with interchange-plus pricing becomes a critical necessity to decouple your revenue from the aggregator’s premium and regain granular control over your profit margin.

The Customer LTV Impact of Frictionless, Multi-Method Payment Options

Payment infrastructure is often mistakenly viewed only as a necessary cost center, but it is fundamentally the final and most critical gatekeeper of Customer Lifetime Value (LTV). A truly frictionless, multi-method payment experience minimizes the cognitive load and psychological friction at the point of sale. When high-intent customers encounter a slow gateway, unexpected redirects, or a lack of their preferred payment method (especially mobile wallets or regional options), the resulting abandonment is a direct erosion of LTV that extends far beyond the single lost transaction.

For high-growth stores, the flexibility you offer at checkout is a signal of trust and a powerful driver of retention. Implementing a modern payment processor that can handle diverse methods not only boosts initial conversion but also lays the technical groundwork for repeat purchases. Here are the key technical and strategic functions that directly impact LTV:

- Secure Tokenization: Utilizing payment processors that offer secure tokenization to store customer payment details allows for true one-click re-ordering, drastically lowering friction for subsequent high-margin purchases.

- Buy Now, Pay Later (BNPL) Integration: The strategic inclusion of BNPL options often raises Average Order Value (AOV) by removing the immediate financial barrier, effectively increasing the LTV contribution of the initial transaction.

- Local and Mobile Wallet Support: Supporting regional payment wallets (e.g., Apple Pay, Google Pay, specific country-focused methods) caters to specific high-value customer segments, demonstrating platform accessibility and professionalism, which is essential for global or scaled domestic growth.

Ready to take your e-commerce to the next level?

The technical nuances of payment gateways, processors, and aggregators are just the surface. If your checkout conversion rate is flatlining, your hidden processing fees are quietly gutting your profit margin, or your limited payment methods are actively deterring high-LTV customer segments, the root problem is a strategic one, not a technical checklist item. The choice of a payment solution is a core growth decision, and if you’re only focused on the lowest nominal fee or the quickest setup, you are guaranteed to be losing revenue to payment friction, high decline rates, and an unoptimized customer journey that suppresses Customer Lifetime Value (LTV).

To move beyond an expensive, fragmented checkout and architect a system that drives maximum Profit, Retention, and LTV, you need a holistic, data-driven strategy. We act as a strategic extension of your in-house team, and our process begins with rigorous, no-guesswork, data-driven & conversion-focused audits. We pinpoint the exact structural leaks in your payment, tracking, and automation systems—ensuring your entire tech stack works in concert to maximise ROAS and long-term growth. If you are ready to pivot from basic fee analysis to a payment strategy designed for exponential revenue scale, book a free consultation today.